Five things to look for

If someone pitched you IUL, whole life, infinite banking, tax-free retirement income, or premium financing, do not judge the policy by the headline illustration. Check the structure.

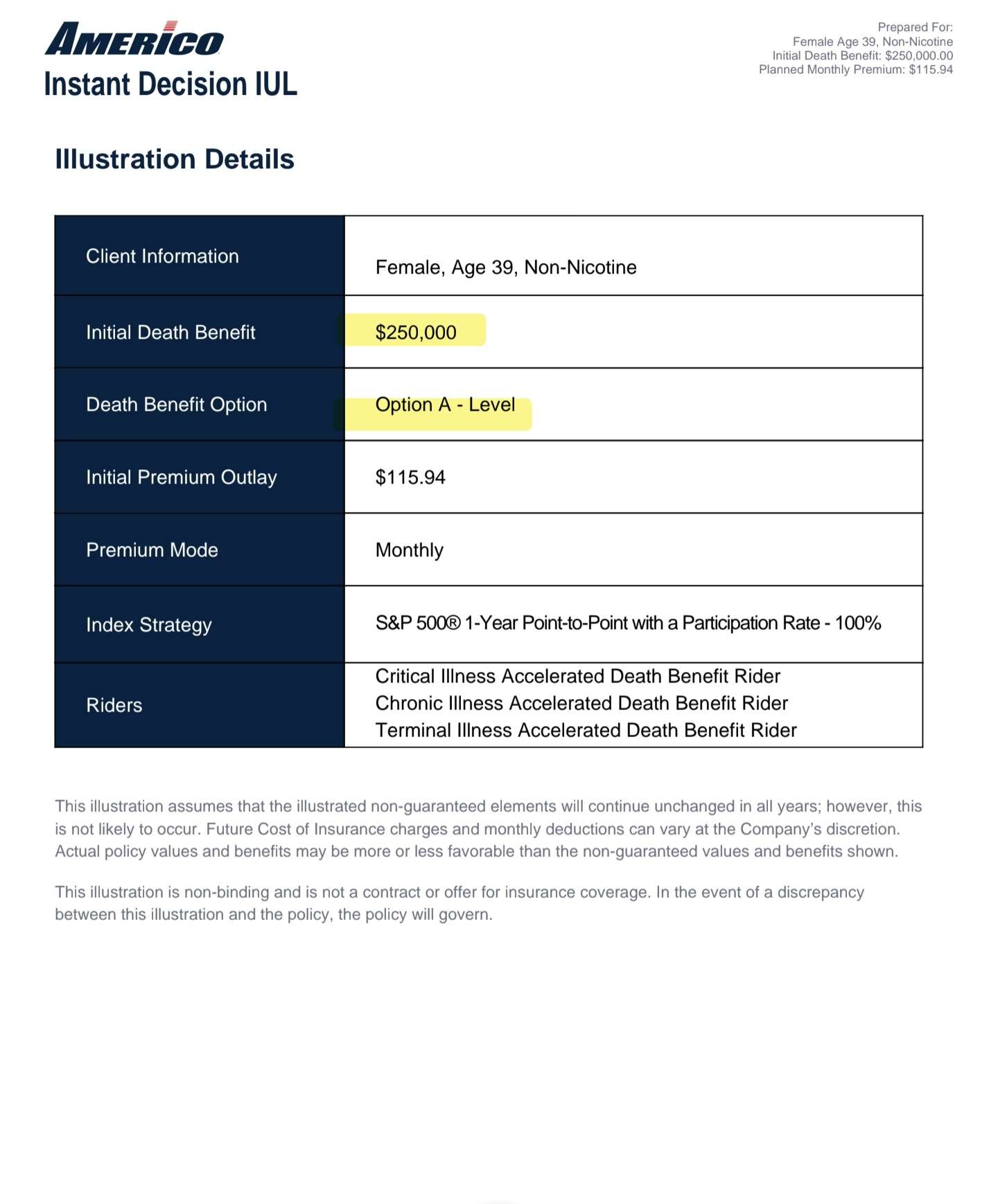

Option A level death benefit

A level death benefit can force more of your premium into insurance cost instead of cash value. For cash-value-focused designs, you usually want the least amount of death benefit allowed for the premium, not a giant fixed death benefit that drags the policy down.

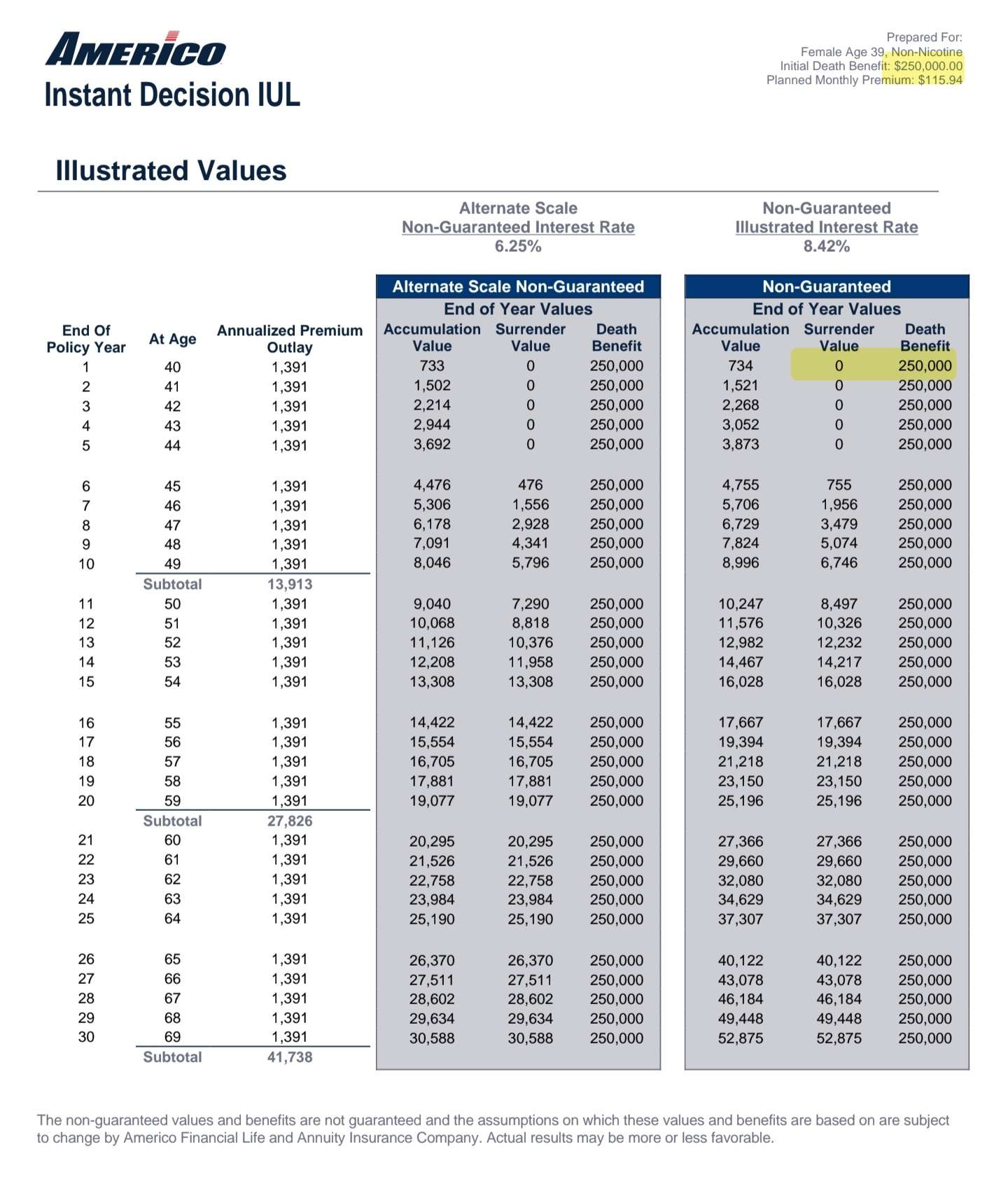

Zero cash value in year one

If the first-year cash value column says zero, that is a red flag. You paid real money. A properly designed cash-value-focused policy should show meaningful cash value early, not make you wait years just to see your own premium show up.

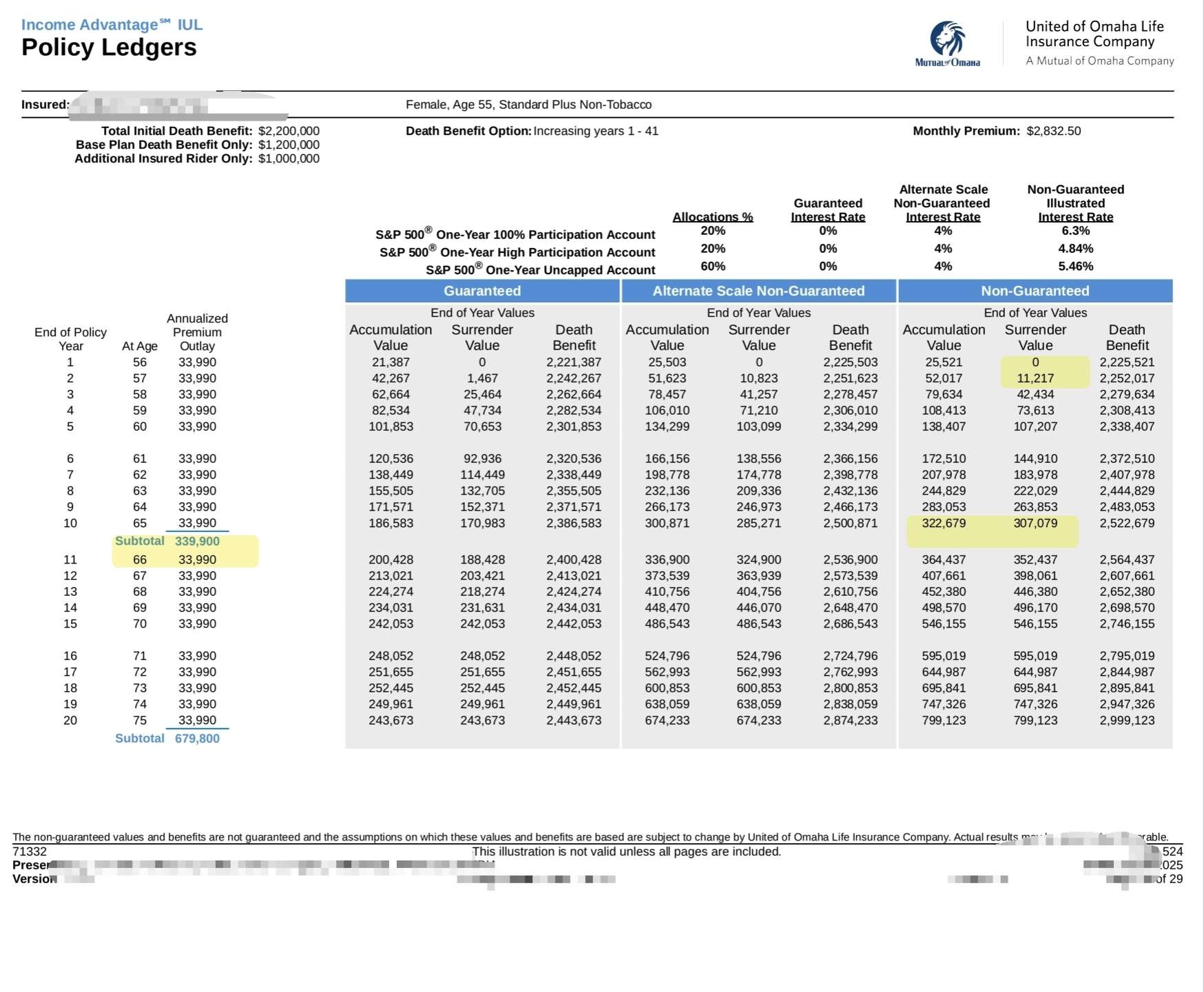

Year-seven break-even

Look at year seven and compare the cash value to how much premium you put in. If you are still far underwater after seven years, the policy may be overloaded with death benefit, charges, or commission-heavy design.

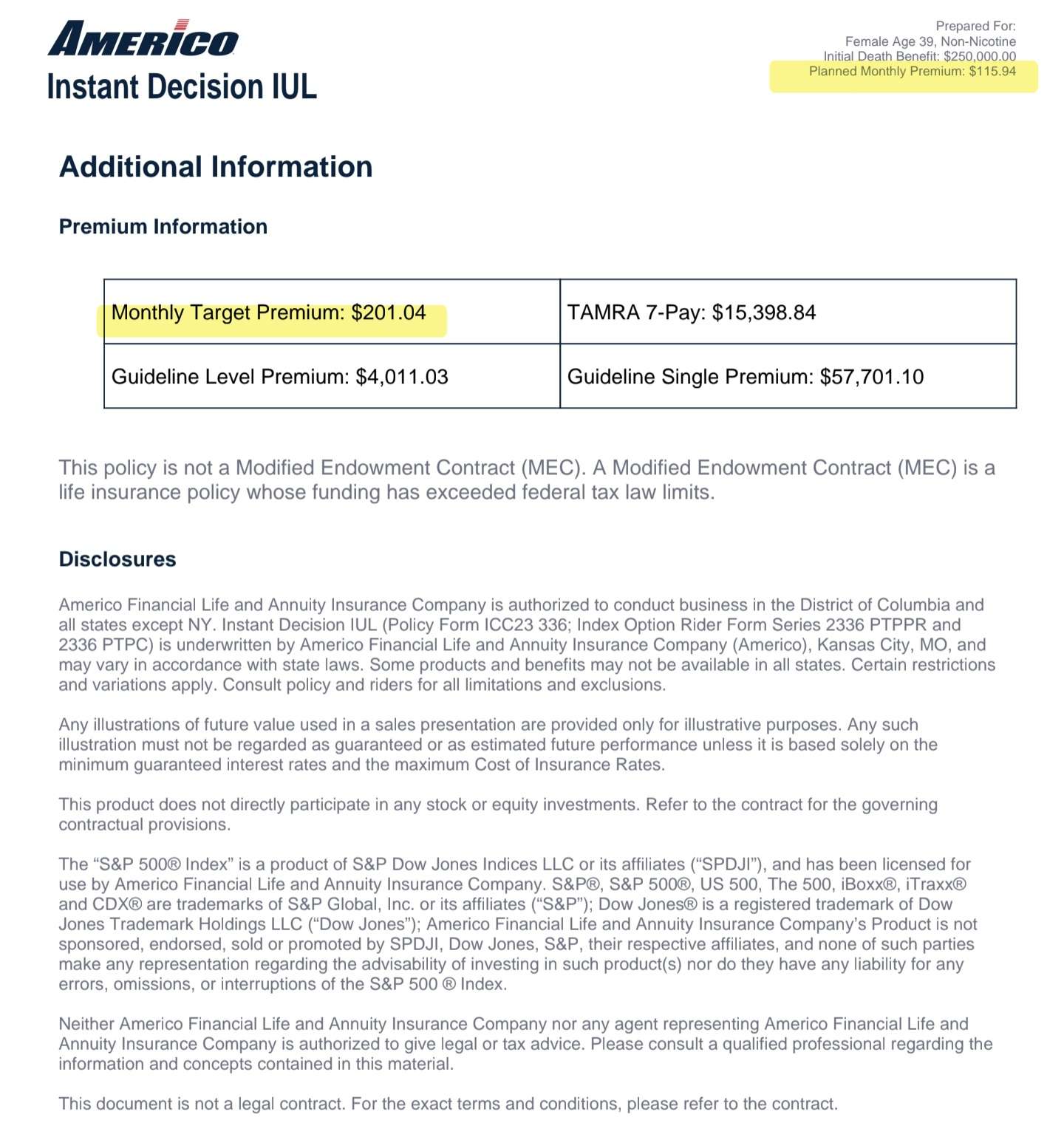

Target premium versus cash value accumulation

Target premium is the amount that usually drives a large part of the agent compensation. If the target premium is above 33% of the total first-year premium, the policy is not set up correctly for cash value. Example: if the annual premium is $6,000 and the target premium is $3,000, the target premium is 50%. That is higher than 33%, which means the policy was likely written for commission, not for value. In a cash-value-focused design, the rest should be excess premium doing the real cash accumulation work.

A flat round-number death benefit

If the death benefit is a round number like $500,000, $350,000, or $200,000, ask why. A cash-value policy designed around Internal Revenue Code Section 7702 often lands on a specific, non-round number because the death benefit is being minimized relative to the premium. A clean 7702 design is usually math-driven, not picked because the number sounded nice.

Good fit if…

You were sold a cash value life insurance policy as a retirement account, tax-free income strategy, infinite banking plan, or safer alternative to market accounts.

Where these red flags show up

These are example illustration pages with the important areas highlighted. The point is not to attack one carrier. The point is to teach people where to look before they keep funding a policy they do not understand.

A policy can be legal and still be poorly designed.

The question is not just whether the policy exists or whether the carrier is reputable. The real question is whether the design matches the job you were sold.

If the goal was cash accumulation, early liquidity, or future policy loans, the illustration should prove it. If most of the money is being eaten by insurance costs and charges, you need to know that before you keep funding it.

Bring these if you have them

Request your Cash Value Policy Review

No external message is sent by this page until you submit the form. A real person reviews the request before any follow-up.

If you had even one of these five red flags, book an appointment and we can walk through whether the policy is fixable, should be left alone, or needs a deeper review. If you know the carrier, product name, premium amount, death benefit, and current cash value, include those details.